Shocking: Jim Chanos Makes Bold Bitcoin and MicroStrategy Bet

In a surprising turn, renowned short-seller Jim Chanos, known for his past skepticism towards cryptocurrencies, has unveiled a unique arbitrage play involving Bitcoin and MicroStrategy. This move marks a significant shift for Chanos and offers a fascinating perspective on current market dynamics.

Jim Chanos Takes Opposing Stances on Bitcoin and MicroStrategy

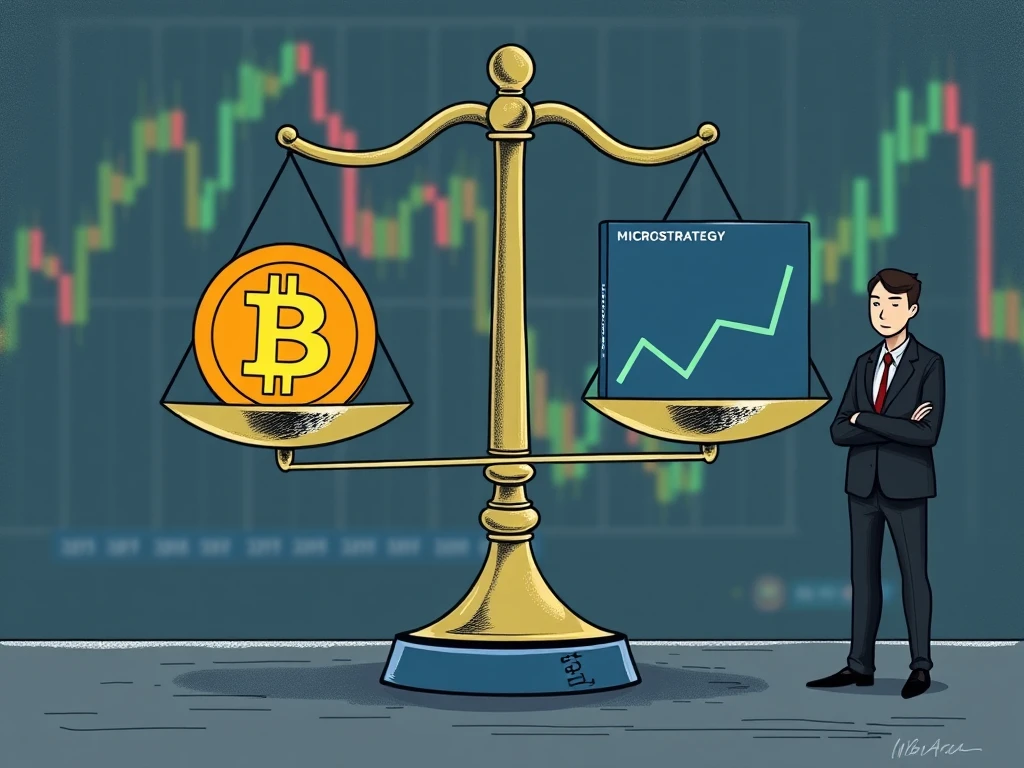

During the Sohn Investment Conference in New York, Jim Chanos disclosed his latest trading strategy: shorting shares of MicroStrategy (MSTR) while simultaneously buying Bitcoin (BTC). He described this as an arbitrage opportunity, essentially seeing a price mismatch where buying Bitcoin directly is cheaper than gaining exposure through MicroStrategy’s stock.

Chanos believes that MicroStrategy’s stock price reflects a premium for providing corporate exposure to Bitcoin, a premium he considers excessive. He suggests this approach encourages other companies to follow suit, aiming for a similar market valuation boost, which he finds “ridiculous.”

Understanding the Arbitrage Play: Shorting MicroStrategy, Buying Bitcoin

Chanos’s crypto investment strategy is based on the premise that investors are overpaying for Bitcoin exposure when they buy shares of companies like MicroStrategy that hold significant BTC on their balance sheet. By shorting MSTR, he bets its price will fall, while buying BTC directly, he bets Bitcoin’s price will rise or at least maintain its value relative to MSTR’s premium.

- Shorting MSTR: Betting the stock price will decrease, potentially as the perceived premium for its Bitcoin holdings diminishes.

- Buying Bitcoin: Gaining direct exposure to the asset itself, bypassing the corporate structure premium.

- Arbitrage Goal: Profit from the perceived mispricing between the value of MicroStrategy’s Bitcoin holdings and the company’s stock market capitalization.

This move suggests that holding Bitcoin through a corporate wrapper reflects excessive speculation and mispricing of risk, particularly driven by retail investor enthusiasm for indirect exposure.

The Risky Business of Short Selling MicroStrategy

While Chanos sees an opportunity, shorting MicroStrategy has proven challenging for many investors. Those who bet against the company in 2024 faced significant losses, estimated at around $3.3 billion, as the stock price surged. Since beginning its Bitcoin accumulation in 2020, MicroStrategy’s stock has seen a remarkable 1,500% increase, significantly outpacing broader market indices.

As of May 2025, MicroStrategy holds approximately 568,840 Bitcoin, valued at roughly $59 billion. The company’s strategy, championed by Michael Saylor, aims to leverage its Bitcoin treasury to potentially become a leading publicly traded equity.

Jim Chanos’s Evolving View on Bitcoin

Jim Chanos has not always held a favorable view of Bitcoin. In 2018, he famously called it a “libertarian fantasy,” questioning its store-of-value potential in extreme economic scenarios. He also criticized the broader crypto sector, labeling it the “dark side of finance” in 2023 and expressing skepticism about the motives behind promoting spot Bitcoin ETFs.

Despite these past critiques, his current action suggests he now sees value in holding Bitcoin directly, especially when compared to the perceived overvaluation of companies like MicroStrategy.

A Look at Jim Chanos’s Short Selling History

Jim Chanos gained prominence for successfully shorting Enron before its 2001 bankruptcy. However, his short-selling record is not without challenges. Notably, his bearish stance and short position on Tesla, announced in 2016, resulted in significant losses as Tesla’s stock experienced massive growth. This highlights the inherent risks associated with short selling, where potential losses are theoretically unlimited if the asset’s price continues to rise.

Conclusion: A Noteworthy Crypto Investment Strategy

Jim Chanos’s decision to short MicroStrategy and buy Bitcoin is a notable development in the financial world, blending traditional short-selling tactics with the volatile crypto market. It underscores his belief in a valuation disconnect between direct Bitcoin ownership and corporate wrappers. While the success of this specific crypto investment strategy remains to be seen, given the risks involved in shorting a high-momentum stock like MSTR, it certainly provides a compelling case study on market premiums and investor behavior in the age of corporate Bitcoin treasuries.